At Your Service

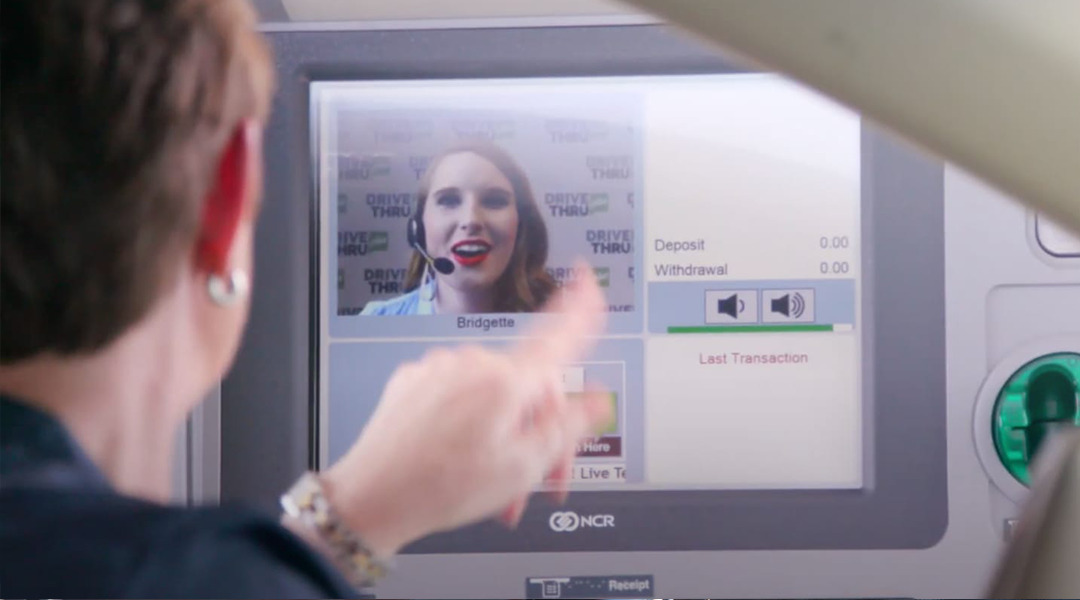

At Your Service DRIVE THRU plus

DRIVE THRU plus

ACH News

Preparing for faster payments

Important ACH News

SAME DAY ACH EFFECTIVE SEPTEMBER 23, 2016:

Currently, most ACH payments are settled on the next business day. There are many uses of ACH payments, however, for which businesses and consumers could benefit from same-day processing. This NACHA rule change will enable ACH Originators that desire same-day processing the option to send same-day ACH transactions to accounts at any receiving financial institution (RDFI). The Rule includes a “Same Day Fee” on each Same Day ACH transaction so that RDFIs would recover, on average, their costs associated with enabling and supporting Same Day ACH.

The Rule will enable the option for same-day ACH payments through new ACH Network functionality, without affecting existing ACH schedules and capabilities.

Originating financial institutions (ODFIs) will be able to submit files of same-day ACH payments through two new clearing windows provided by the ACH Operators (Note: The actual ACH Operator schedules are not determined by the NACHA Operating Rules.

• A morning submission deadline at 10:30 AM ET, with settlement occurring at 1:00 PM.

• An afternoon submission deadline at 2:45 PM ET, with settlement occurring at 5:00 PM.

Generally, all types of ACH payments, including both credits and debits, will be eligible for same-day processing. Ineligible items include international transactions (IATs) and high-value transactions above $25,000. Eligible transactions account for approximately 99% of current ACH Network volume.

All RDFIs will be required to receive same-day ACH payments, thereby giving ODFIs and Originators the certainty of being able to send same-day ACH payments to accounts at all RDFIs.

RDFIs will be mandated to make funds available from same day ACH credits (such as payroll Direct Deposits) to their depositors by 5:00 PM at the RDFI’s local time.

To allow financial institutions and businesses to acclimate to a faster processing environment, as well as to ease the implementation effort, these new capabilities will become effective over three phases beginning in September 2016. More information will be distributed to outline the Bank’s plan for offering Same Day ACH.

Important Update on Unauthorized Entry Fees:

In 2014, the NACHA membership approved a rule establishing an Unauthorized Entry Fee. Under this Rule, an ODFI will pay a fee to the RDFI for each ACH debit that the RDFI returns as unauthorized (i.e. a return that uses a return reason code R05, R07, R10, R29 and R51). The amount of the Unauthorized Entry Fee will be $4.50 per unauthorized returns. This fee was based on results of a Receiving Depository Financial Institution (RDFI) cost study performed by an independent third party on behalf of NACHA. This new fee will become effective beginning with such return entries that have a Settlement Date of October 3, 2016. According to this Rule, the initial fee amount will be effective for three years, and then evaluated for any potential adjustment.

Reversals: Complying with ACH Network Rules

An Originator may Initiate a Reversing Entry to correct an Erroneous Entry previously initiated to a Receiver’s account. The Reversing Entry must be Transmitted to the ACH Operator in such time as to be Transmitted or made available to the RDFI within five Banking Days following the Erroneous Entry. ACH Originators may reverse an ACH File or Entry that:

a) Is a duplicate or an Entry previously initiated by the Originator or ODFI

b) Orders payment to or from a Receiver different than the Receiver intended to be credited or debited by the Originator;

c) Orders payment in a dollar amount different than was intended by the Originators;

d) Is a credit PPD Entry satisfying each of the following criteria:

I. The credit PPD Entry is for funds related to a Receiver’s employment;

II. The value of the credit PPD Entry is fully included in the amount of a Check delivered to the same Receiver at or prior to the Receiver’s separation from employment; and

III. The credit PPD Entry was Transmitted by the Originator prior to the delivery of the Check to the Receiver.

The Originator must make a reasonable attempt to notify the Receiver of the Reversing Entry and the reason for the Reversing Entry no later than the Settlement Date of the Reversing Entry. For a credit PPD Entry, the Originator must notify the Receiver of the Reversing Entry at the time the Check is delivered to the Receiver.

Technical Requirements: The word “REVERSAL” is required to be placed in the Company Batch Header to indicate the item is a reversal. NOTE: It is important that to comply with the NACHA Operating Rules that Originators and Third Party Senders of Originators understand their obligation to comply with this Rule and change procedures accordingly.

Receive Our Exclusive E-newsletter

Subscribe

If you would like to receive more tips and articles like these, please sign up to receive our E-newsletter. Money Matters is a quarterly newsletter exclusively for our business customers. This e-newsletter was created with YOU in mind.

In each issue of Money Matters, you’ll get:

Interesting articles to help you be more successful, information on upcoming events and seminars, profiles of Bank of Tennessee employees, practical tips to enhance your business, and much more.

Business Tool Kit

Bank of Tennessee wants to help your business succeed. We’ve created this exclusive Business Tool Kit to provide helpful information for our business customers.